SAS and Kamakura

On June 27, 2022, SAS – the global AI and analytics leader – acquired Kamakura Corporation, a leading provider of risk management software, information and consulting. As a result of the acquisition we can now provide an unparalleled suite of integrated risk solutions, particularly concerning asset liability managment (ALM) and other essential solutions for the financial services industry. SAS has scaled resources to support Kamakura products, enabling SAS resources and selected specialized Partners. The Kamakura products are becoming an integrated part of the SAS Risk platform.

TROUBLED COMPANY INDEX®

The Troubled Company Index ® measures the percentage of 42,500 public firms in 76 countries that have an annualized one-month default risk of over one percent.

DAILY

KRIS Default Probabilities versus

Legacy Ratings

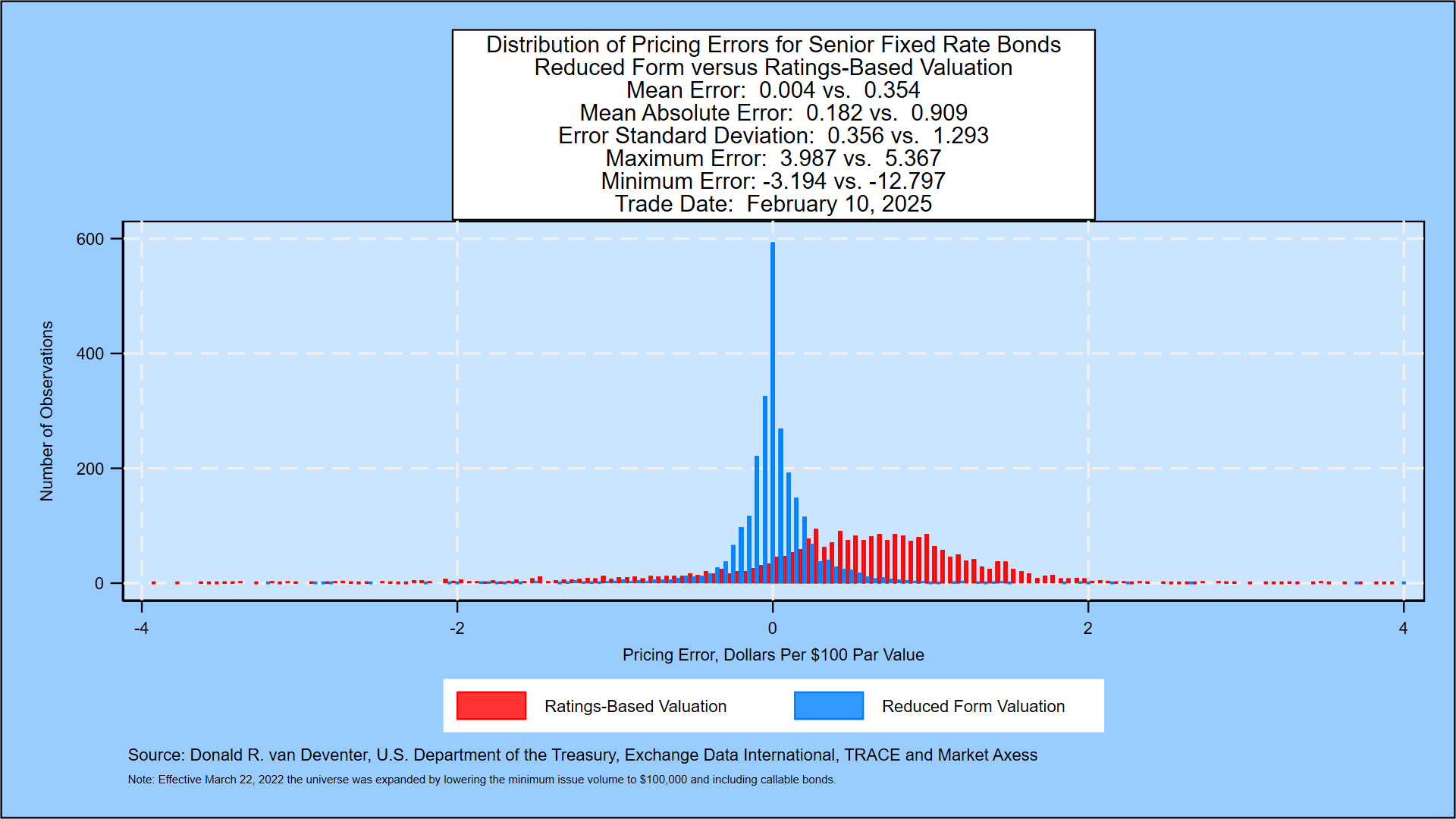

SAS Daily Bond Performance Attribution

KRIS Daily Default Probability and

Bond Cross-Validation

RESEARCH

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, January 2, 2026

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the most important paper in financial economics in the last 50 years.” The Center for Applied Quantitative Finance provides the risk-neutral and...

SAS Weekly Treasury Simulation, January 2, 2026: Measuring the Term Premium in U.S. Treasuries

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of being in this range is 0.29% higher than the probability of being in the 0% to 1% range. Treasury 2-year yields moved to 3.47% this week from...

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, December 26, 2025

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the most important paper in financial economics in the last 50 years.” The Center for Applied Quantitative Finance provides the risk-neutral and...

SAS Weekly Treasury Simulation, December 26, 2025: Yield Level Probabilities from 6 Months to 10 Years

Summary The most likely range for 3-month bill yields in 10 years remained at the 1% to 2% range this week. The probability of being in this range is only 0.02% higher than the probability of being in the 0% to 1% range. Treasury 2-year yields moved to 3.46% this week...

HJM++© Correlated Government Yield and Foreign Exchange Rate Simulations for Asia-Pacific, Europe and North America, December 12, 2025

The Heath, Jarrow and Morton [1992] framework for simulation and valuation using risk-free interest rates has been called “the most important paper in financial economics in the last 50 years.” The Center for Applied Quantitative Finance provides the risk-neutral and...

COMMENTARY

The Narrowing Definition of “Winner”

December capped a year in which headline growth and risk-on positioning coexisted with rising under-the-surface strain—a late-cycle mix that kept markets calm while widening the gap between credit “winners” and “losers.” Continuing the trends of outperformance, the US...

Three Years Post ChatGPT

November 30th marked the three-year anniversary since the public release of ChatGPT. Back then, the S&P 500 stood at 3,950 compared to its most recent close of 6,849 – a 73% increase and $24T gain in total market cap. Meanwhile, Nvidia’s most recent net income...

Record Highs

October was another month for the history books. Equity markets notched new record highs: S&P 500 added $17 trillion since the April lows, Nvidia became the first $5T market cap company, Amazon surged almost 10% post earnings recording largest one-day market cap...

Non-conventional Fed actions lowered default risk in the short-term—but what’s coming next?

NEW YORK October 1, 2025: The U.S. markets have become conditioned to seeing the Federal Reserve step in whenever negative conditions appear to worsen. Of course, many see the Fed’s interventions as a safety net – as indeed they are during times of crisis. But...

Tariffs: Learning from History to Chart a Path to the Future

NEW YORK September 2, 2025: Successful investing is the art of filtering out noise so that you can focus on signals leading to long-term gains. But how do you do that when markets are constantly jolted by changing tariffs—and shifting sentiment about their potential...

EVENTS

- September

- 07–10 SEP | 2025 MSATA (Midwestern States) Annual Meeting

- 09 SEP | SAS Innovate on Tour, Mexico City

- 11 SEP | SAS Innovate on Tour, Sao Paulo

- 15–16 SEP | MoneyLIVE North America

- 16-17 SEP | Nordic Financial Crime & Sanctions Forum

- 17 SEP | Palm Beach Economic Crimes Unit 2025 Financial Institution and Law Enforcement Annual Training Seminar

- 22–24 SEP | MoneyLIVE North America

- 30 SEP | SAS Innovate on Tour, Los Angeles

- 30 SEP | ACAMS Carolinas Chapter, 5th Annual AML and OFAC Symposium

- October

- 02 OCT | ACAMS Carolinas Chapter Symposium | Charlotte, NC (Banking-AML/Fraud)

- 08–09 OCT | RiskLive NA

- 14–16 OCT | ITC Vegas

- 29–30 OCT | Balance Sheet Management USA